-

- Research to Correct the Problems of the Regulators of

Client’s Risk

-

- Kenneth Sullivan, Ph.D, Dean Kashiwagi, Ph.D, P.E., Blake Carroll,

Matthew Lee, and Marie Kashiwagi

- Performance Based Studies Research Group (PBSRG)

- Arizona State University

- Tempe, AZ

-

The bonding and insurance surety industry has had difficulty

regulating risk in the construction industry. They have had a constant

increase in payouts and premiums due to increased construction contractor

nonperformance in the price-based construction environment. This paper

reviews the mechanics of the construction contractor funding model, the

construction surety model, and the construction industry structure. The risk

of the surety industry is attributed to volume and price based practices. It

identifies that the surety industry is caught in the same predicament as the

contractors: They are trying to regulate. The paper proposes changes in the

surety model, and a research proposal to test the hypothesis that sureties

will be successful if they minimize the risk of nonperformance.

-

-

Key Words:

Construction Industry Sureties, Price Based Practices, Construction Risk,

Construction Performance

-

-

-

- Introduction

-

- The construction industry represents 8% of

the U.S. gross domestic product according to the U.S. Census Bureau. The

construction industry employs over 6 million workers in over 1.9 million

construction companies, with revenue of $916 billion (Engineering Technology

2004). With the most competition seen than ever before in recent years and

increased expectations by project owners, the construction industry is one of

the most risky fields of business there is today (SIO 2004). With this risk,

there comes the need for insurance and bonding companies to underwrite and

guarantee the completion of construction projects. Over the past thirty years

the construction industry has moved from a performance-based sector to a

price-based sector. This move has had an enormous impact on the construction

industry. When the focus of the industry was on performance, contractors were

more attentive to the quality of work and reputation. A contractor’s

reputation was more important and based on past performance. If a contractor

did not perform, the chances of future work was slim. The construction

industry clients are concerned primarily with three performance areas: having

the project completed on-time, within the proposed budget with minimized

change orders and meeting the quality expectations of the owner. When the

construction industry moved into the very competitive price-based environment,

contractor motivation shifted from quality to price, making performance an

inconsistent attribute when selecting a contractor in today’s price based

marketplace.

-

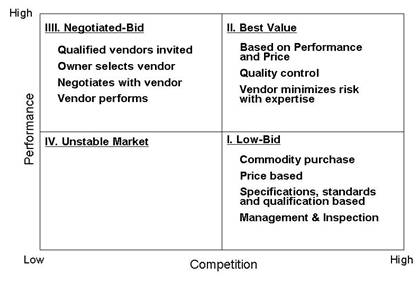

- Figure 1 shows that high performance

contractors are asked to not use their expertise and bid a construction

project with the lowest possible price. Because risk is the reciprocal of

performance, the client’s directive to the contractors is to bid the lowest

possible price and maximize the potential risk. If the contractor is being

asked to maximize risk, the client is giving the competitive advantage to

those contractors who are:

-

-

1.

More likely to pass the risk to the client.

-

2.

Lower performers who cannot predict risk of construction projects.

-

3.

Volume based.

-

4.

Have a lower quality of work.

-

-

|

- Figure 1: Construction

Environment (Kashiwagi 2002)

|

-

-

- Price

Based Environment in the Construction Industry

-

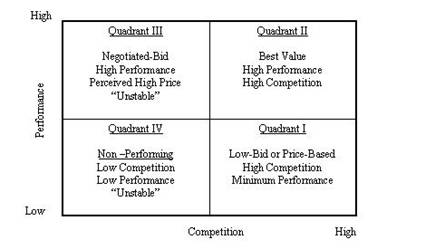

- The construction industry can be simply

explained by the Construction Industry Structure (CIS) model (Figure 2) which

explains the industry based on performance and competition. The three major

segments of the industry are the negotiated bid (high performance, limited

competition), the best value award (high performance and competition), and the

price based sector (high competition, minimal performance). The risk is

highest in the price-based sector (risk is the opposite of performance).

Surety companies maximize their profit when the construction industry is in

the high performance environments.

-

|

- Figure 2: Construction

Industry Structure (Kashiwagi 2002)

|

-

- The construction industry is not in the

performance environment. Rather it is in the price-based sector based on the

following measurements and observations:

-

-

-

-

Construction performance is very inconsistent.

-

-

The craftsperson skill and construction coordination/supervision level

is decreasing.

-

-

Contractor profits are relatively low for a high-risk industry (1-5%).

-

-

Contractor turnover is high, and not limited to new contractors.

-

-

Surety payouts are high.

-

-

Insurance companies participating in construction surety are

consolidating and having a more difficult time surviving.

-

-

Construction bonding and insurance rates are increasing.

-

-

Both contractors and sureties are taking a volume-based approach

instead of risk adverse position.

-

-

The contractor and the client are in an adversarial or “win-lose”

relationship. The client is requesting the contractor for the minimal

performance for the lowest price. The contractor is following the client’s

instruction and maximizing instead of minimizing the client’s risk. The

client tries to minimize that risk by managing and inspecting the contractor

and using performance bonding.

-

-

-

Volume Based Philosophy of the Price Based Environment

-

|

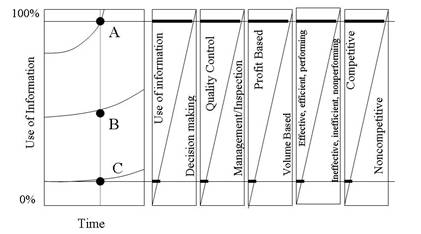

- Figure 3: Rate of Change

and Kashiwagi Solution Models (KSM)

|

-

- Figure 3, the Change Rate Chart and two

way Kashiwagi Solution Models (KSM), shows that the difference between the low

risk (high information party) Type A and the high risk (low information party)

Type C. The two way chart shows the relative difference of the two parties in

relation to the amount of information that is being used. For example in the

first KSM, it shows that the Type A uses a maximum amount of information

(longer line) before the event to minimize risk. The Type C uses very little

information (shorter line). The Type A practices quality control. The Type C

practices very little quality control, and feels much more comfortable being

managed and inspected. The Type A does less work and maximizes profit. The

Type C maximizes the amount of work and minimizes their profit. This is

called commodity work, or price based work. The risk is greater with the Type

C work. Figure 3 then defines the price-based work as:

-

-

Minimizing the use of performance information.

-

Minimizing quality control (that comes with expertise).

-

Maximizing management and inspection (which is required with inexperienced contractors).

-

Volume based work with lower profit margins.

-

Higher risk.

-

- Both the contractor investment/funding

model and the surety model are both volume based (increased risk in a

noncommodity industry). There are two major participants in a construction

contractor: the owner or investor, and the contractor personnel (construction

managers and craftspeople). Construction companies are usually created by the

investor/owner’s investment funding. The funding is used to purchase the

required assets, personnel and services to start the construction company.

The contractor is then allowed to bid projects ten times the size of their

financial worth. In the vernacular of insurance companies, this is defined as

risk.

-

- The surety companies are in business to

make a profit by underwriting contractors who can perform (finish on-time,

on-budget, and meet the requirements of the client). If the contractor cannot

perform due to a lack of personnel who have the appropriate experience,

financial stability, or have maximized their capability on other projects, it

is in the best interest of the sureties to deny the contractor a performance

bond. In this manner, the sureties become the regulator of construction

performance in the industry.

-

- When the contractor makes a 1% profit, the

investors are actually making a 10% increase of their investment. Therefore,

the investors do not mind if the contractor makes a 1% profit of the project

bid. However, if a contractor does not make a profit, the investor’s loss is

exponential. It is therefore in the best interest of the investor for the

contractor to do more work, minimizing the chances of not making a profit. If

the contractor is making only a 1% profit, the contractor’s personnel are put

under extreme stress to ensure that the profit is maintained. At a 1% profit,

any mistakes in scheduling, bidding, unforeseen events, poor coordination, or

construction errors can easily erase the profit. To maintain the profit

margin, the contractor will attempt to increase its volume and pass the risk

to all other parties. The high turnover rate of contractors, the poor

performance record, and inability to increase the quality of work validates

the concept that although investors are satisfied with a low profit margin,

the low profit margin places the contractor personnel at extreme risk.

-

- It is the sureties’ function to regulate

which contractors are not a risk (allowed to do ten times the amount of work

as their assets). It is common practice that the sellers of the performance

bonds for the surety companies are independent sales personnel who are paid

based on commission. They are therefore volume oriented and not risk

adverse. They themselves have no risk. After being paid their commission,

they are no longer involved in the construction. This coupled with the

concept that the sureties do not make their profit on the underwriting but by

investment of the fees in the stock market, also encouraged the sureties to be

volume oriented. These practices have brought risk to the sureties and

insurance companies when the stock market significantly declined. Also, as

the volume oriented construction industry became riskier, payouts increased to

almost 60% of premiums, putting sureties at risk and forcing indiscriminate

higher insurance and bonding rates to the contractors. The volume-based

approach of both the contractors and sureties has done little to stem the

nonperformance in the construction industry (Surety Bonds 2003).

-

- As a result of the volume based approach,

bonding and insurance companies are underwriting contractors based on project

size rather than past performance and the ability of the contractor to

minimize risk. Underwriters still have brokers working to sell based on

volume. Brokers stand between companies that want to purchase insurance and

the companies selling insurance, taking a commission for services rendered.

Not only are these brokers paid on commission, but they also occasionally

receive kickbacks, which is paid only if the broker places a certain amount of

business with a particular insurer. (The Economist Newspaper 2004)

-

-

- Bonding and Insurance Industry Losses

-

- The problem on the contract side of the

surety business started appearing in 2000 when there began to be a large

number of failures by subcontractors that had taken on more work than they

could handle. This produced $600 million in losses for sureties, of which

$400 million was pushed off to re-insurers. After more than a dozen years of

profitability, a recession began in the spring of 2001, which slowed down the

construction industry and sent 255 public companies into bankruptcy, most of

which were users of commercial surety bonds. As contractor failures

increased, sureties paid nearly $1.8 billion in claims in 2000 and 2001

according to The Surety Association of America (SAA). Then the attacks on the

World Trade Center hit insurers for roughly $40 billion (Krizan et al. 2002).

-

- In reaction to severe losses, many

sureties exited the business, some increased rates, and all took a more

disciplined approach with underwriting and capacity. A few surety companies

consolidated or left the market altogether. Sureties became more cautious

about bonding large-scale, long-term contracts. It was no longer a buyer’s

market. The more conservative surety companies continued to do business as

always but with an eye on underwriting and claims (Surety Bonds 2003). Today,

the commercial and contract surety markets are having trouble with capacity

restrictions due to reinsurance. In the past seven years, insurance and

bonding rates have increased. In those seven years, the losses incurred

jumped from 25.6% to 69.8%, a total increase of 52.1% (see Table 1).

-

- Table 1:

- Aggregate Insurance Expense Exhibit Data Calendar

(1998-2002)

|

- Calendar Year

|

- Premiums Written

|

- Premiums Earned

|

- %

|

- Losses Incurred

|

- %

|

- 1998

|

- 2,930,601

|

- 2,824,405

|

- 100

|

- 723,292

|

- 25.6

|

- 1999

|

- 3,399,321

|

- 3,077,088

|

- 100

|

- 902,319

|

- 29.3

|

- 2000

|

- 3,363,352

|

- 3,218,469

|

- 100

|

- 1,491,053

|

- 46.3

|

- 2001

|

- 3,473,090

|

- 3,330,161

|

- 100

|

- 2,748,424

|

- 82.5

|

- 2002

|

- 3,754,733

|

- 3,513,742

|

- 100

|

- 2,454,258

|

- 69.8

|

-

|

-

|

-

|

-

|

-

|

-

|

- TOTAL

|

- 16,921,097

|

- 15,963,865

|

- 100

|

- 8,319,346

|

- 52.1

|

-

-

- More than 80,000 contractors failed during

1990-1997, leaving private and public construction projects with liabilities

exceeding $21.8 billion (Construction Chart Book 2002). Surety was a $3.2

billion industry in 2001 and there were nearly $2.2 billion in gross losses

(State Of The Surety Market 2002). With these dramatic increases in surety

losses, the construction industry’s stability and sustainability is

questionable if it remains in the price-based sector. Underwriting standards

declined consistently from 1992 to 2000 with new carriers fighting for market

share and becoming more aggressive, resulting in poor loss ratios for the

industry (State Of The Surety Market 2002). Bonding and insurance companies

looking for profitability and sustainability must re-evaluate their

operations.

-

-

- Impact on Construction Industry

Sustainability/Profitability

-

- Some insurers have reviewed the losses on

their construction book of business and have decided to stop underwriting

construction risks. Not only do other insurers not want to write new

construction accounts, but they are issuing cancellation notices to

contractors in the primary construction class codes, the majority of them

being General Contractors and Artisan Contractors in trades such as

excavation, concrete, carpentry, drywall, and roofing. Some contractors are

looking away from insurance companies as well. Contractors as well as other

companies are buying less coverage. Policy limits for insurance in all

industries declined 9.4% in 2003 and 14.5% over the past three years,

according to a survey by broker Marsh and

McLennan Cos.,

New York City. Construction insurance costs are near the top for all

industries. For $1 million of coverage it costs on average $20,620 (SIO

2004). Many contractors’ premiums have climbed substantially, more than

doubling in some cases. Even though contractors are paying more than double

for their policies, their umbrella coverage in most cases is half what it used

to be. This is forcing many smaller construction company owners to downsize

by cutting managers pay and making unwanted layoffs.

-

- Ten years ago the top ten sureties had 20%

of the business and today they have 40% (Krizan et al. 2002) As the loss

ratios have increased bonding and insurance companies have had to merge or

leave the surety business completely. Bonding and insurance agencies have had

to limit the coverage with numerous exclusions with hopes to spread the risk (SIO

2004). Contractors now must find numerous insurance policies to cover a

project, which in the past was covered by a single insurance company.

Therefore, construction companies are paying higher premiums for many

insurance policies with less overall coverage.

-

- Contractors on mega projects ($200 million

and up) will experience the greatest change in their bond programs (Surety

Bonds 2003). Not only are the large projects affected, small contractors who

perform well and produce quality products will also be affected.

-

-

- Hypothesis

-

- The authors are proposing that sureties

cannot increase their profitability in the price- based sector. The structure

of the environment is increased risk, a higher cost of overhead in an attempt

to manage and inspect the risk. This includes increased bonding and insurance

costs. Sureties are not profitable in underwriting contractors with high

risk. The paper proposes that sureties can be more profitable in the best

value, high performance environments.

-

-

- Methodology

-

- The methodology would be to identify

contractors who either take the approach of a high performance contractor who

minimizes their workload or is working for a best value client who is

providing an efficient, “win-win” environment for the contractor. The

methodology would include minimizing any high risk or volume based practice

previously used. This includes giving lower rates on volume-based work or

using independent brokers paid on commission.

-

-

- Proposed Research

-

- One of the co-authors is being asked to

present to the National Sureties Meeting for the second year in a row. The

first presentation explaining the risk of the price based construction sector

surprised the majority of attendees (independent sales personnel, sureties,

insurance company personnel). Their reaction confirmed that

sureties/independent sales personnel don’t understand the mechanics or risk of

the construction delivery process. The objective of this year’s presentation

is to propose a research project with a surety/insurance company. The

research effort will be to design the mechanism for the following:

-

-

Identify high performance/low risk contractors who can be

regulated with performance information.

-

Identify contractors who are high performing and working for best value

clients who have use a risk minimization delivery process.

-

Identify how the sureties can minimize their

risk on an ongoing basis by motivating the contractors to continuously

improve.

-

Identify the mechanism that will replace the

independent broker who works on commission.

-

- The proposed research methodology

includes:

-

- Identification of a high performing

contractor or best value based client. Identification will include a

collection and analysis of past performance information, ability to

effectively assess risks on contracts, and project performance in ongoing

operations. The same would hold true for the selection of best value based

clients – the best value system used by the selected clients would have to

show consistent results of procurement through high performing contractors.

Delivered work would have to be consistently on-time, on-budget, no GC

generated cost change orders, and high customer satisfaction.

- Surety Results from Best Value Pool –

once the high performing contractors and best value clients have been

identified the research would move to tracking the results of the sureties

profit from these research pools. The research pool would consist of profit

based contractors that do not operate under volume-based returns. If the

profit results from the high performing research pools showed gains over

normal operations the research would move into the phase of implementing

change.

- Adjustment and Testing of Surety

Practices – once a statistically significant difference in surety

performance has been established between the research pool and normal

operations adjustments and testing of those adjustments to normal operation

would commence. Adjustment could include, though are still in development,

considerations for volume based work, broker payment, tracking of

performance information, etc. The developed mechanism will assist or

replace the broker-on-commission practice.

- Final Analysis of Surety Adjustments –

after a decided duration (2-3 years) the results will be analyzed to

determine if the surety improved and to ensure that the improvement was

caused primarily by the adjustments made and not outside market factors.

-

-

- Conclusion

-

- The regulatory function of the

surety/insurance groups is dysfunctional. The observations and measurements

of the surety company and construction industry show high risk and low

performance. The authors are proposing that increasing rates in the

price-based sector will not stabilize construction industry performance. The

price based delivery process that uses minimum standards, management, control,

and inspection by client’s representatives, which sets an adversarial

relationship and maximizes the opportunity for less experienced contractors,

puts the sureties at risk. It is proposed that the sureties move their

business to the best value environment and use the practice of performance

information and risk minimization to maximize their profit. This proposal

will be further discussed with potential surety research partners.

-

-

- References

-

- Ames, W. (2002) Secrets of a Surety.

The Associated General Contractors (AGC) of America.

-

- Bonding and Insurance Trouble. (2004,

February 26) Engineering News Record (ENR). URL

http://enr.construction.com/opinions/editorials/archives/040126.asp

-

- Construction Chart Book. (2002) The

Construction Chart Book (3rd ed). The U.S. Construction Industry

and Its Workers.

-

- Engineering Technology Curricula & Courses

(2004, September 1) Construction Management.

Western Carolina University: Engineering

Technology. Accessed on October 1,

2004, at http://et.wcu.edu/ET-CC_CM-gen-info.htm.

-

- Grenier, D. (2001) Construction Insurance

in 2001 and Beyond: A Wake-Up Call! C-Risk Inc. Consultants in Risk

Management. URL

www.c-risk.com/Articles/dlg_ins_wake-up_01.htm

-

- Kashiwagi, D. (2002) Best Value

Procurement (2nd ed). Performance-Based Studies Research Group

-

- Korman, R. (2004, January 26) Rising

Prices, Shrinking Policies Generate Waves of Uncertainty. Engineering News

Record (ENR), 252 (4), 22-27.

-

- Korman, R. and Illia T. (2003, August 4)

Insurance: Policies for Defects Axing Key Elements. Engineering News Record (ENR),

251 (5), 12-13.

-

- Krizan W., Korman R., Tulacz G., and

Ichniowski T. (2002, February 11) Bonding Businesses Going For Broke?

Engineering News Record (ENR). URL http://enr.construction.com

-

- Schubert L. (2001, July) Surety Industry

Addresses Increases in Surety Losses. URL

http://www.irmi.com/Expert/Articles/2001/Schubert07.aspx

-

- SIO (2004, November 15) Surety Bonds At

Work. Surety Information Office (SIO). URL

www.sio.org/html/sbw

-

- SIO (2003) “Why Do Contractors Fail?

Surety Bonds Provide Prevention & Protection.” SIO Surety Information Office.

-

- Surety Bonding: The Importance of

Surety Bonds in Construction.

(2003, October 15) MORGAN Insurance. URL

http://www.sio.org/html/importance.html

-

- The Economist Newspaper. (2004, October

21) Just How Rotten?. URL http://www.economist.com

-

- State Of The Surety Market (2002,

December) Accessed on October 31, 2004, from http://www.cybersure.com/documents/surety/surety%20market%20-%202002.pdf.

-

- Surety Bonds 2003 (2003) Accessed on

October 31, 2004, from http://enr.construction.com/resources/special/archives/surety_2003.asp

-