(pressing HOME will start a new search)

![]()

![]()

![]()

THE USE OF PROBABILITY AND EXPECTED UTILITY THEORY FOR RISK MANAGEMENT IN CONSTRUCTION

Jac de Jong

Department

of Construction Science

Texas

A&M University

College

Station, Texas

|

Contractors in the construction industry are facing a multi�tude of decisions involving uncertainty and risk. This pa�per deals with a methodology for developing a more organized and consistent approach to decision making. Use is made of probability theory in order to assess uncertainty, while risk is incorporated by using the expected utility theory. Both theories are briefly discussed. Two specific problems are worked out to examplify the methodology. First, when a choice exists between different projects, what project to bid on, and secondly what profit margin to apply. And although two problems are dealt with, the methodol�ogy is applicable to many problems in the industry. Judge-�mental factors are involved in the process, which makes the methodology far from perfect. However, the method pro�vides a consistent and rational approach to decision making and is therefore seen as an improvement over what is being used today. Keywords: Construction, Risk, Uncertainty, Utility, Probability. |

Introduction

The

majority of industries are governed by a few large capital intensive

organizations, controlling most of the industry's assets. Although the heavy

construction industry follows more or less the same pattern, the building

industry, on the contrary, consists of a conglomeration of diverse specialty

companies, brought together when a new project is initiated. The industry is

fragmented to the extent that a general contractor may require some 15 to 20 odd

sub�contractors. The diversity of these organizations of sub�contractors makes

the coordination for planning and sched�uling by the general contractor

extremely complex when a project is newly acquired.

Besides

these complexities many uncertainties exist in terms of the reliability of the

multitude of the different bid prices obtained from many sub-contractors, the

securing of a skilled labor force, as all of them are very labor intensive, and

the allocation of labor and equipment resources with the acquisition, delivery

and installation of building materials.

The

market itself is mostly unpredictable, strongly com�petitive and fluctuates

with the economic conditions 1o�cally, regionally and nationally, not to

mention the often extreme seasonal variations in the different regions.

Most

projects are obtained on a competitive bid basis, usually one project at a time,

and independent of all other projects, either in progress or still waiting to be

tendered. Hirings and layoffs are therefore quite often the order of the day.

This requires that the industry must have a built-in flexibility in order to

cope with these fluctuations in the labor force to increase or decrease

personnel quickly and efficiently, while still maintaining a skilled skeleton

labor force to maintain stability.

Inflation

and interest rates are unpredictable for projects of long duration. To obtain

insurance, bid and performance bonds, for incorporation into the bid price, can

sometimes be difficult and laborious, specifically under the present economic

constraints.

Labor

unrest always looms on the horizon. The industry is therefore probably one of

the most volatile, competitive and, judging by the bankruptcy rate, least

profitable busi�ness in existence.

These

difficulties raise questions such as what projects to bid on to maintain a

balanced operation for the company, who are the competitors and how many are

there, how to establish the profit margins and what does it depend on in order

to be successful in obtaining a project. In answering these questions, decisions

need to be made on a responsible and rational basis in order to minimize risk

and maximize profits. In the majority of cases decisions are not made in a

consistent and organized manner, in particular the finalizing of the bid

proposal. Therefore, the concepts of both responsibility and rationality are

being lost in the process and for that reason are further explored.

What

is the meaning of "responsible" and "rational" in this

context? According to the "Larousse Illustrated International Encyclopedia

and Dictionary", 1972, pg. 753, it means "fit to be placed in

control". The "Webster's New 20th Century Dictionary", 2nd

Edition, pg. 1543, defines "responsible" as "the ability to

distinguish between right and wrong and to think and act rationally, and hence

accountable for one's behavior".

"Rational"

according to Webster's New World Dictionary of the American Language", 2nd

College Edition, pg. 1179, implies the ability to reason logically as by drawing

conclusions by inferences and often connotes the absence of emotionalism. This

definition uses the word "reason", given as something to think out

systematically by drawing of inferences or conclusions from known or assumed

facts. (Webster's, pg.1183).

Considering

these definitions acting "responsible" is behavioral related and

requires the distinction between right and wrong and may well mean different

things in different cultures. It definitely involves acting on one's own and

being held accountable.

"Rational"

is used in this paper as it is in the Sciences, a systematic progression or a

step by step reasoned and consistent development of coming to conclusions. And,

as in the Sciences, it inherently adheres to a body of conventions that

establishes rational and consistent thinking. What these conventions are and the

calculus of using them will be the subject matter of this paper.

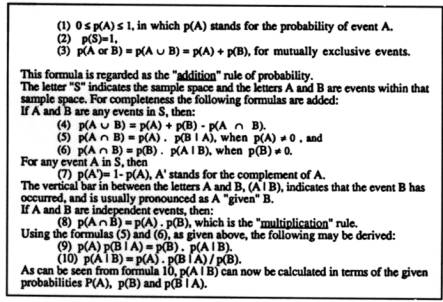

Decision Analysis

Decision

analysis incorporates both uncertainty and risk in the decision making process.

To deal with "uncertainties" use is made of probability theory. It

will be assumed that a basic knowledge of set theory and probability theory have

been acquired. The axioms of probability, with the formules for calculating both

conditional probability and the Bayes' theorem, are given as they relate

directly to the material.

Risk

is incorporated through the use of Utility theory, which relates the company's

value system to the risk involved. This value system depends on the

"state" of the organization itself, on the value the owner as an

individual or the corporation as a group places on everything it owns and owes,

including its labor force. Expanding these resources depends on the risk the

company is willing to take, as the taking of risks is directly related to the

return on investment.

In

financial decisions, as for example those made in the bid proposal of a

construction company, uncertainty is assessed using probability theory. Three

different approaches for establishing the neccesary probabilities exist

presently, namely:

The

objective approach,

The

subjective approach,

The

classical approach.

The objective approach is based on the relative frequency of events in repeated experiments. Experiment here, may be interpreted in its broadest sense, as this approach has been taken by the contractor in recording the number and prices for each project.

The

subjective approach gives the probability value as a measure of belief that one

has in the knowledge that exists of the world at that specific point in time.

This may be called experience or intuition.

The

classical approach is based on the fact that events have an equally likely

chance of occurrence, as for example taking a card out of a well-shuffled deck

of cards. These approaches are made operative by using a calculus of probability

based on axioms which will be spelled out further on. (Goldberg, 1986)

Making

decisions is the process of selecting one action from an array of alternative

courses of action with each alternative course of action having a specific

outcome. Each outcome is evaluated in terms of its consequences for either loss

or gain. The "expected outcome" is calculated by multiplying the

outcome, or payoff, with its probabilities for both winning and losing and then

summing the results. An individual can determine the maximum expected value of

the different outcomes that satisfies the proposed goal, in this case,

maximizing the return on investment. It is assumed that an individual will

choose the outcome, that maximizes the expected value, as each outcome is based

on the premise of anticipating the predicted future for each alternative.

The

scale used for measuring these consequences or uncertainties is given by a

number between zero and one, which indicates the value of the judgements of the

relative likelyhood for these predictions. These numbers must satisfy the axioms

of probability, given as follows:

|

|

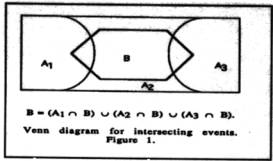

This

concept can be expanded upon in a more generalized form. The sample space S is

divided into 3 mutually exclusive events. Such a division is called partitioning

of the sample space. An event B intersects with all of the 3 events, A,, Az, A;,

as shown in the Venn Diagram below, figure 1, then the event B may be calculated

as the union of 3 mutually exclusive events.

|

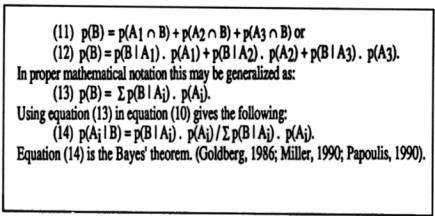

|

In

terms of probabilities and using the addition rule, the probability of B may be

stated as follows:

|

|

This

process may be described as the adjustment of the probabilities of Ai when the

probabilities of B are known. One way of establishing the probability of B is by

performing experiments. The "experiment" used here is the recording of

previous bid proposals submitted by the competitors. When the probability p(Ai)

does incorporate this experimental data, then it is called the "a

posterior" probability of Ai, otherwise it is the "a priori"

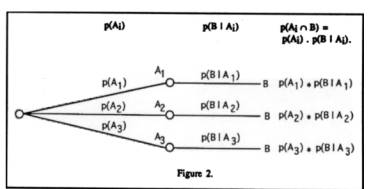

probability. Graphically this may be depicted as follows, figure 2:

|

|

It

may also be mentioned that independence of events A and B is obtained when p(A I

B) = p(A) and p(B I A) = p(B), which means that the probability of A is not

altered by the probability of B, when p(B) is known. This concept is important

as independence of events make the use of the "multiplication" rule

possible.

Utility

theory, on the other hand, attempts to describe man's behavior in which

decisions involving risk are made. It consists of a preference system, called

utility, that ranks the preference among different alternatives. Its scale is

totally arbitrary. These preferences adhere strictly to axioms in order to be

consistent and rational. These axioms are briefly stated as follows:

Axiom#1:

Comparability: alternative A1 preferred to A2 or A2 to A1 or otherwise both are

equally preferred.

Axiom

#2: Transitivity: A 1 preferred to A2 and A2 to A3 then A 1 preferred to A3.

Axiom

#3: Continuity: A I preferred to A2 and A2 to A3 then there exists a probability

p for which a sure amount for A2 is equivalent to the gamble p times A1 and (1-p)

times A3.

Axiom

#4: Compound lottery: may be substituted for a simple lottery, which is obtained

by multiplying the compound lottery by its probabilities.

Axiom

#5: Monotonicity: comparing two outcomes for two alternatives, in which the

outcome with the highest probability is preferred.

These

are given here without proof and the reader is referred to the literature for

further examination. (Lifson, 1982; Watson, 1987; Kleindorfer, 1993).

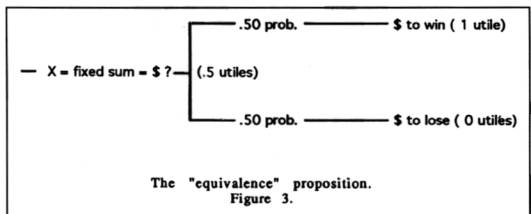

Based

on these axioms the theory establishes a functional relationship, called a

"utility" function, between the value of an outcome and its rank on a

scale of preferences.

The

function is obtained by making "equivalence propositions" between a

lottery and a fixed sum of money in the following manner, figure 3, or the fixed

sum of money is given and the probabilities need to be determined.

|

|

By

varying the amounts of money for the lottery and the fixed sum, multiple points

of the function can be established and the curve plotted.

The

dollar value of each alternative is then scaled against the utility function and

its utility value, measured in utiles, determined. By calculating the

"expected" utility value for each outcome the contractor will prefer

the outcome with the highest expected utility. (Lifson, 1982; Watson, 1987;

Kleindorfer, 1993).

Two

specific problems are considered, although this methodology is applicable to

many problems in the construction industry.

First:

the problem of establishing what project to bid on out of a choice of three.

Second:

what profit margin to consider regardless of what project is chosen.

Assume

that three projects are simultaneously up for tender and that the following

hypothetical information is obtained in regard to the three projects.

For

project 1 the contractor has a 75'/. chance of winning S 150,000.00 and a 25%.

chance of losing 530,000.00.

For

project 2 there is a 80% chance of winning S I 10,000.00 and a 20%. chance of

losing $20,000.00.

For

project 3 a 90%. chance of winning $80,000.00 and a 10% chance of losing

$10,000.00.

The

dollar amounts for winning or losing are the estimated quantities established by

the contractor.

The

given chances or probabilities are "subjective" probabilities, in

other words a gut feeling the contractor has about the chances of winning or

losing.

To

be able to chose the best alternative, in this case one of the three projects,

use is made of the concept for optimization of the expected monetary value (EMV).

The EMV is calculated in the usual manner by adding the amounts one stands to

win and lose multiplied by respective probabilities.

The

calculations are performed in table 1:

|

|

When

strictly going by the concept of the EMV, the contractor should choose the

alternative, which maximizes the return on investment. Project I provides the

maximum expected profit of $105,000.00 and thusly should be the one to select.

It provides also the greatest risk opportunity in that there exist a 25% chance

of losing $30,000.00.

The

contractor is risk averse and wants to postpone the decision on which project to

bid. An utility function needs to be established to incorporate the contractor's

value system and attitude towards risk. In order to be able to construct the

curve for the utility function, two approaches are followed to obtain the

"equivalence propositions".

the

"certainty equivalence" and

the

"probability equivalence" approach.

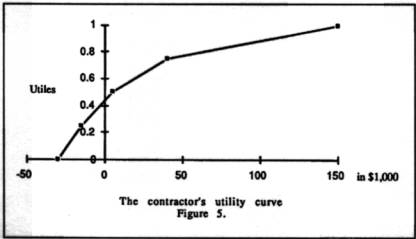

First

the range of the amount of profit and loss is calculated and the extreme dollar

values determined. The maximim amount to be gained is $150,000.00, the maximum

amount to be lost is -$30,000.00. These amounts are plotted on the X-axis and a

scale determined.

The

utility value for the $150,000.00 is set to one utile, and for the -$30,000.00

to zero utiles. A scale is established between 0 and 1, using equal intervals,

on the Y-axis.

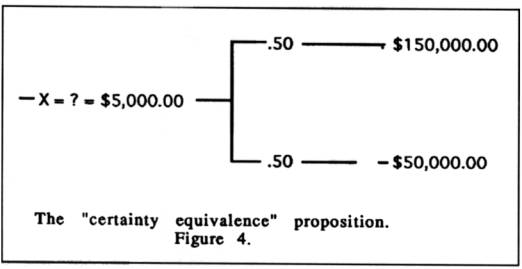

For

the "certainty equivalent" approach the following hypothetical

proposition is made. There exists a 50-50 chance of making $150,000.00 or losing

$30,000.00 against getting for sure an amount of x dollars. This amount needs to

be determined by the individual or organization involved, in this case the

contractor. Establishing this amount indicates that the individual is

indifferent between taking the sure financial award or the lottery with the 50-50

chance of winning or losing. (Kleindorfer, 1993) Graphically the proposition is

depicted in figure 4 as follows:

|

|

Suppose

that the sure amount is $5,000.00. This corresponds to the.5 mark on the utility

scale, and establishes one point on the utility curve. This point signifies that

the contractor is indifferent between either getting the $5,000.00 for sure or

the 50-50 chance of winning the lottery of $150,000.00 or losing $30,000.00.

This

process is continued by now considering $5,000.00 with a utility value of .5 and

the $150,000.00 with an utility value of 1. If for example, the contractor is

willing to settle for $40,000.00 for sure or the 50-50 chance for the lottery of

making $150,000.00 or making $5,000.00, then the utility value of the $40,000.00

is halfway between.5 and 1 on the utility scale and is equal to .75.

The

same approach is followed for the proposition of the 50-50 chance for the

lottery of winning $5,000.00 with a utility value of.5 or losing $30,000.00,

with a utility value of 0. It is assumed that the contractor is indifferent if

the amount is -$15,000.00, which is equivalent to an utility value of .25. Five

points of the utility curve are now obtained and the function can be

established.

In

order to generate a utility function use can be made of the PROC NLIN command in

the SAS language. This requires the establishment of 15 to 20 points before the

curve can be generated and the equation formulated. This seems hardly practical

as each point is obtained by making a judgement between a lottery and a fixed

amount of money. Besides, the preferences on the utility scale have arbitrary

values in the sense that one alternative is preferred over another qualitatively

but not quantitatively. How much more one alternative is preferred over the

other is not specified.

The

accurate "e - functions" found in the literature, (Lifson, 1982),

required the determination of at least 15 individual points before such an

equation could have been formulated.

Another

method of generating a curve is by using the "cubic splines

interpolation" method in the Mathcad software. This method fits a curve to

a set of points so that the first and second derivatives at the given points of

the curve are continuous, creating a series of cubic equations between the

points. No actual single equation is established.

Utility

values are determined as the intersection with the ordinate for the profit

amounts on the X-axis and the utility curve. The utility function for the

contractor is drawn by hand as sketched in figure 5.

|

|

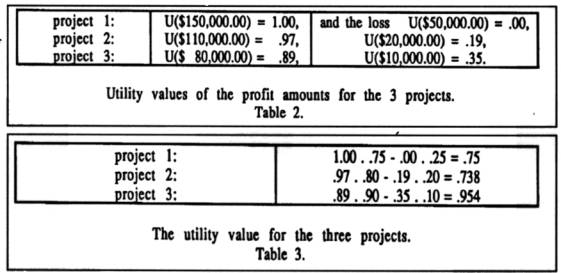

By

scaling the amounts of profits/loss to be made for each project on the utility

function, the utility values for each profit/loss margin is measured. These

values are (table 2):

The

expected utility value is determined for each of the three projects and the

maximum utility value observed, table 3.

|

|

Table

3 provides the answer to the question of what project to bid on. The project to

be considered for tendering is the one with the maximum utility value of .954,

which is project 3. The above utility figures give a good indication of the

preference the contractor has for bidding projects involving risk.

The

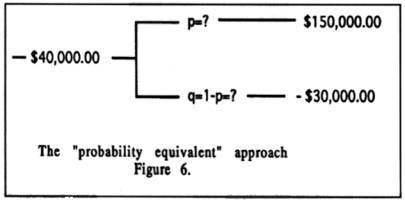

"probability equivalent" approach follows the same pattern with this

difference that in the proposition the amount for sure is given, but the

probabilities for the lottery need to be determined.

This

approach is graphically depicted in figure 6:

|

|

The

probability p is so determined and the process follows through in the same way

as before with the "certainty equivalent" approach. This is another

way for determining the same utility curve.

The

second problem of what profit margin to incorporate in the bid price will now be

addressed.

In

the example to be used, the cost estimate of the contractor for previous bids is

taken as the base-line for establishing the markups of the bids for the

competitors.

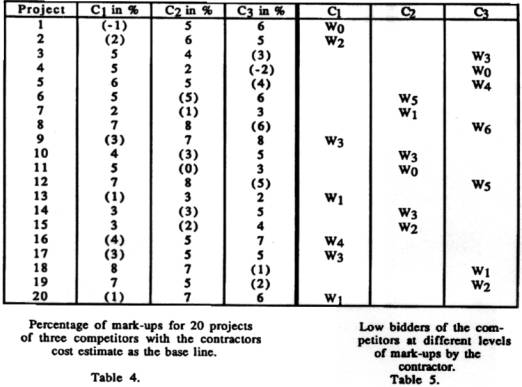

Of

the 20 bids recorded for each competitor, assuming that the three competitors

all bid on the same projects, the percentage over/ under the cost estimate is

given in table 4.

It

is also assumed that the 20 jobs listed are all more or less of the same size

and price range, so that the effect of job size does not influence the profit

margins. Each bidder is also equally desirous of obtaining work, although the

percentages of the mark-ups should reflect this trend.

The

low bidder for the three competitors for each project is denoted by having

brackets around the percentage number as indicated in table 4. For example,

competitor 1 is the low bidder for project 1, while for project 3 competitor 3

is the low bidder. Table 4 gives the low bidder for each project.

|

|

The

contractor's bid proposal, for each mark-up level ranging from 0 to 6 %, is

compared with the lowest bid of the competitor for that project, as given in

table 4. The opportunity for being successful in obtaining the project is so

determined.

At

the cost, or the 0% level of the mark‑up, the contractor's bid is compared

with the lowest bid of the three competitors for each project. It may be

observed that competitor 1 is still the low bidder with the bid proposal being 1

% below the cost estimate of the contractor. This is indicated in table 5 by WO

denoting a low bid or a win for competitor 1 at the 0% level of the cost

estimate for the contractor. This process is repeated for the 1 % level of the

cost estimate with the results shown in table 5. The W 1 in the C2 column for

project 7 indicates that if the contractor adds a mark-up of 1 % competitor 2 is

still the low bidder. Continuing in the same manner, for all levels of the mark-ups,

table 5 is completed.

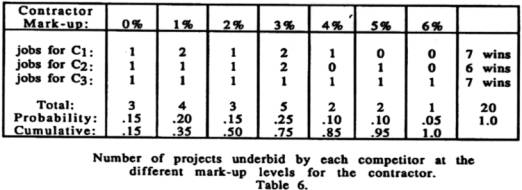

Table

6 summarizes the results of table S, giving at each mark-up level for the

contractor the number of projects underbid by each of the competitors. Thus at

the 2% level of mark-up competitor 1 underbid the contractor on 1 more project,

namely project 2, and the contractor has thus been underbid an accumulative

total of 4 projects, projects: 1 (WO), 2 (W2), 13 (W 1), and 20 (W 1). Table 6

has so been tabulated, and the cumulative probabilities included.

|

|

The

numbers in the cumulative row in table 6 are the probabilities that the

contractor will lose the bid against three competitors. The probabilities for

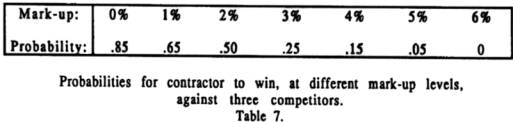

the contractor to win against three competitors is obtained by deducting the

cumulative probabilities from 1 and given in table 7.

|

|

The

probabilities in table 7 are obtained from the data given in table 4 by

calculating the actual relative frequencies, thus representing the best possible

estimate obtainable for these probabilities.

Other

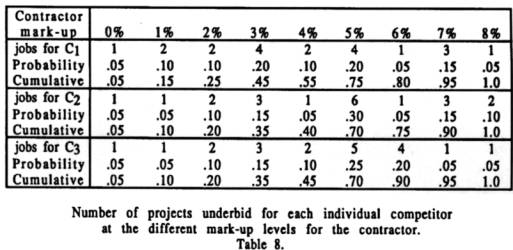

methodologies can be found in the literature. One of the methodologies makes use

of the multiplication rule and establishes for each individual competitor the

probability of winning a project and multiplying these individual probabilities

in order to obtain the winning probability for the contractor. (Park, 1966).

These may be calculated by following the same procedure as before and compare

the contractor's bid proposal with the one for each of the competitors on an

individual basis.

The

data for that comparison is available from table 4 and the results for each

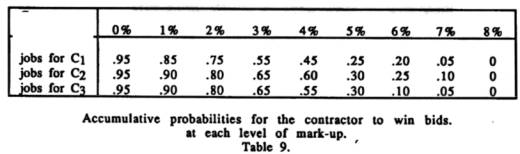

competitor, are given in table 8. The cumulative probabilities for the

contractor to win bids against the individual competitor C1, C2, and C3 are

summerized in table 9 by deducting the cumulative probabilities in table 8 from

1.

|

|

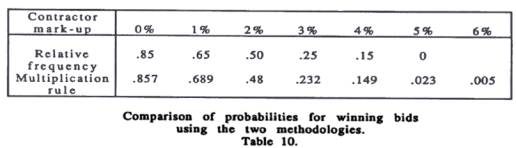

By using the multiplication rule, the probabilities for winning against each individual competitor may be multiplied together in order to obtain the probabilities for the contractor to win a bid against three competitors.

At

the 0% mark-up level the contractor's probability of winning would then be .95 .

.95 . .95 = .857. At 1 %: .689, 2%:.48, 3%:.232, 4%:.149, 5%:.023, 6%:.005.

These

values are compared with the ones in table 7, which were obtained by using the

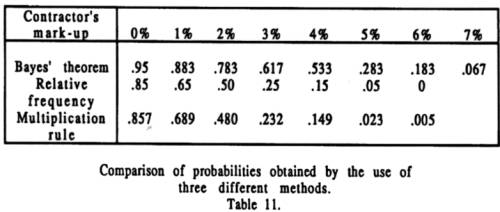

relative frequency approach, and are summarized in table 10.

|

|

|

|

Although

these figures are remarkably similar, the multiplication rule requires that

events are independent. The contractor's bid price and those of the three

competitors are not independent events. On the contrary they are mutually

exclusive and exhaustive, which means that the occurrence of one event precludes

the occurrence of the other and that only one of the events can occur. When

events are mutually exclusive they cannot be independent. (Hays, 1973).

Independence exist only if the probability of one event is not influenced by the

other.

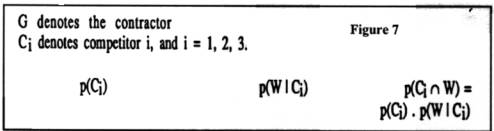

Assume

that G denotes the contractor, then for independence to hold p(G I C 1) = p(G),

for all Ci's, i = 1, 2, 3. This indicates that if the probability of C 1 is

known the probability of G would stay the same and the multiplication rule would

be valid, which is not the case.

This

controversy brought about the suggestion that the Bayes' theorem would be a

better approach towards establishing the probabilities for the contractor to win

against the three competitors. (Lifson, 1982). In order to use the Bayes'

theorem the events need to be dependent and mutually exclusive. Although not

individually independent, pair-wise independence may well exist. (Goldberg,

1986), in which case this scenario may be described as a pair-wise comparison

among the pairs (G - C1), (G - C2) and (G - C3). For the multiplication rule to

be valid independence must then exist among the pairs (C 1 - C2), (C 1 - C3) and

(C2 - C3).

Using

the Bayes' theorem this pair-wise comparison can be shown diagrammatically in a

probability tree as given in figure 7.

|

|

The

.95 probabilities in figure 7 are obtained from table 9 at the level of 0% mark-up.

The

"a priori" probability for each competitor is 1 /3, as each has an

equally likely chance of occurring, if the assumptions hold.

The

"a posterior" probability is then calculated by using the Bayes'

formula as follows: p(C1 /W 1) = p(C1) , p(W1 / C1) / (p(C1) . p(W1 / C1) +

p(C2). p(W2 / C2) + p(C3). p(W3 / C3)]. (Goldberg, 1986).

The

probability of winning for the contractor, at the level of 0% mark-up, against

the three competitors is the summation of W1 +W2 +W3 = 1/3 . (.95) + 1/3 . (.95)

+ 1/3 . (.95) = .95. This amounts to nothing more then averaging the individual

probabilities for the three competitors. This is accomplished for each level of

mark-up and the results tabulated in table 1.

The

same table gives the comparison with the probabilities in table 10.

Theoretically, pair-wise independence has not been dealt with abundantly in the

literature, and its validity here is questioned when the results are compared

with the ones given in table 11.

|

|

For

purposes of father analysis the probabilities, obtained from the methodology of

the actual determined relative frequencies, will be used.

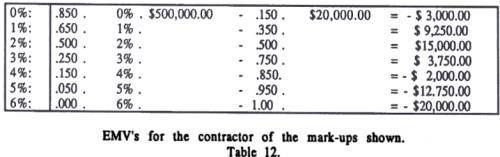

Assume

that the contractor's cost estimate is $2,500,000.00 and that the loss of

investment, if bid is lost, is $20,000.00.

To

be able to chose an alternative, in this case one of the projects, again use is

made of the concept for optimization of the expected monetary value (EMS, in the

manner as used before.

In

tabular form the EMV's are summerized in table 12:

|

|

As

can be seen from the calculations, the maximum amount of expected profit is

$15,000.00.

Adhering

again to the concept of the EMV, the contractor should chose the alternative,

which maximizes the return on investment, which is the one with the $15,000.00

profit at the 2% level of the mark-up. The probability of winning the bid is .5

or 50%. However the contractor is anxious to employ the available resources and

may decide not to persue this particular option. Instead the contractor will be

looking for the alternative that best serves the objectives for keeping his work

force productive and taking the appropriate kind of risk.

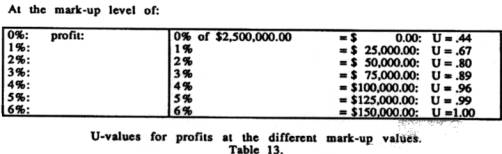

Use

is therefore made of the utility function as previously established in figure 5.

By

scaling the amounts of profits to be made for each level of mark-up on the

utility function, the utility values for each profit margin is measured.

The

utility value for losing the bid is .19 utiles for the $20,000.00, as measured

from the utility curve. Summerizing, these values are given in table 13.

|

|

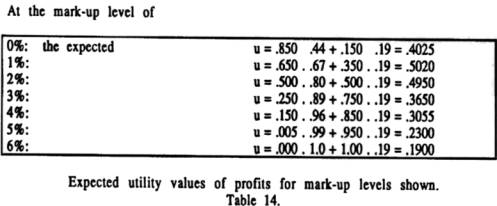

Given

the figures in table 13 the expected utility values can be determined by

multiplying the probabilities of winning and losing with the respective utility

values for the profits as indicated. Table 14 gives these calculations. The

alternative with the highest utility value, which is the alternative at the 1 %

level of the mark-up, is chosen for the bid proposal. As can be seen this

alternative has a probability .650 or 65% of being successful and deviates from

the choice made under the EMV calculations, which was the third alternative at

the 2% level of the mark-up.

|

|

In

conclusion it may be stated that the methodology for establishing probabilities

by using relative frequencies in order for the contractor to win certain

projects appears to be the most feasible, but also the most cumbersome.

Epilogue

In

order to improve decision making a clear rational approach, consistent with the

principles and axioms spelled out herein, is necessary. Uncertainty is involved

in every decision problem to be faced. Probability as a measure of uncertainty

maybe based on both judgmental factors or historical data, as is the case

herein.

The

subject of judgement has its inherent ramifications. But so has the relative

frequency approach. Who is to say that the pattern from historical data will

follow through into the next problem situation, indicating that regardless of

the results obtained judgement still needs to be exercised.

Using

utility theory for risk assessment also has to overcome the hurdles of

judgemental factors by substituting certainty for a lottery. These judgements

are no doubt subject to human error. However these will improve as experience is

gained and this approach is used as a means to provide a consistent and rational

methodology for gaining meaningful experience.

References

Goldberg,

Samuel. 1986. Probability. An Introduction. Dover Publication, Inc., Prentice

Hall, Inc., New Jersey.

Hays,

Wiliam L. 1973. Statistics for the Social Sciences, Holt, Rinehart and Winston,

Inc., New York, N. Y.

Meindorfer,

Paul R, Kunreuther, Howard C., Schoemaker, Paul J. H. 1993. Decision Sciences.

Cambridge University Press, New York, N. Y.

Lifson,

Melvin W., Shaifer, Jr.,Edward F., 1982. Decision and Risk Analysis for

Construction Management. John Wiley & Sons, New York, N. Y.

Miller,

Irwin, John E. Freund and Richard A.Johnson.1990. Probability and Statistics for

Engineers. Prentice Hall, Inc., New Jersey.

Papoulis,

Athanasios. 1990. Probability and Statistics. Prentice Hall, Inc., New Jersey.

Park,

William R 1966. The Strategy of Contracting for Profit. Prentice Hall, Inc., New

Jersey.

Watson,

Stephen R. and Dennis M. Buede. 1987. Decision Synthesis. Cambridge University

Press, Cambridge, U. K.