(pressing HOME will start a new search)

![]()

![]()

- ASC Proceedings of the 25th Annual Conference

- University of Nebraska-Lincoln- Lincoln, Nebraska

- April 1989 pp 39-43

|

(pressing HOME will start a new search)

|

|

AN EXAMINATION OF MEASURING AND REPORTING WORK PROGRESS

|

Neil N. Eldin |

Robert

K Hughes |

| A number of approaches for measuring and reporting work progress is currently being used in the construction industry, but each has certain features that detract from its effectiveness. These detracting features involve the basis on which we measure work progress and the level at which we integrate cost and scheduling data. This paper examines the current approaches to measuring and reporting work progress and identifies major problems in their implementation. The paper also promotes the search for an alternative approach that may prove more advantageous. |

INTRODUCTION

Construction

is the largest industry in the United States. It accounts for twelve percent of

the gross national product, employs approximately five million Americans, and

involves an annual expenditure of almost four hundred billion dollars [1].

Studies have shown that more than ten percent of the construction enterprises in

the United States fail annually due to poorly informed management and

ineffective use of management tools [2].

Although

the need to minimize potential failure in the construction industry has provided

the impetus for the accelerated growth of project management techniques, major

challenges in tracking construction projects still exist. This paper briefly

describes the current practice in measuring and reporting work progress, and

discusses some problems in implementing the current approach. It also suggests

an alternative approach that seems to have the potential for resolving such

problems.

CURRENT MANAGEMENT APPROACH

The

primary purpose of a project control system is to provide management with the

information necessary for decision making. To prove successful time management

of a project, the current practice often focuses on one date, the completion

date of the project. Similarly, it focuses on one cost figure, the total project

budget, as proof of successful cost management. Since these two performance

measures are certain only at the completion of the project, attempts are made to

determine the project's progress and to predict its performance at intermediate

stages. In doing so, management faces two major challenges: 1) measuring work

progress; and 2) integrating cost with scheduling data.

Measuring Work Progress

Two

basic requirements need to be established at the start of a construction project

to enable the quantitative measurement of work progress. These are: 1)

Definition of the level of detail at which progress will be measured; and 2)

Selection of the basis for progress evaluation.

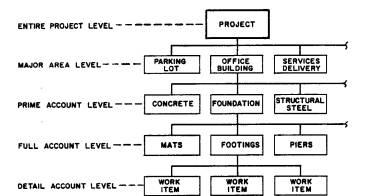

Definition

of the Level of Detail - The work breakdown structure (WBS) is the current

management tool for defining the lowest level of detail at which progress will

be measured on a construction project. The WBS is a concept by which work items

are grouped to establish meaningful relationships among the different levels of

control on the project hierarchy, such as shown in Figure 1. In this manner a

project management team (PMT) can specify the level of detail for the tracking

system adopted. The work items shown on a WBS represent the lowest level of

detail at which project records are kept on a project.

|

| FIG.

1 - Levels of Control on Work Breakdown Structure |

Selection

of Basis for Progress Evaluation - Review of the attempts to quantify work

progress reveals that three bases for progress measurement have been used: 1)

project's expenditures; 2) installed quantities; and 3) earned value.

The

principal assumption in using project's expenditures as a progress measurement

tool is that the ratio of the project's cost-to-date to its total estimated cost

is indicative of the project's progress (percent of completion). It is quite

apparent that a substantial amount of the project's funds can be expended

without any significant progress being realized. This shortcoming directed

attention to the fact that assessment of work progress should be based on actual

quantities installed rather than merely actual expenditures.

Measuring

progress based on quantities installed appeared promising at first. However, the

use of different units of measurement (i.e., pounds, cubic yards, tons, feet,

etc.) was a major obstacle in the application of this method. The different

units did not allow the summation of the progress achieved on subcomponents to

determine the progress of a work item. To determine the project's overall

progress, the summation of progress achieved on different work items was not

possible without assigning weight factors to each item and using the weighted

percent complete (WPC) method [3]. The WPC method entails lengthy and cumbersome

calculations that limits its effectiveness.

It

was also realized that although the quantity of concrete placed on the first

floor of a skyscraper is equal to that placed on the top floor of the same

building, the cost and time for placing each of these two identical work items

are significantly different. Pipe work, structural steel, and piling are other

examples of work items for which the unit cost and unit time vary significantly

based on elevation, size, diameter, and metallurgy, among other factors. For

such items reporting quantity installed could be misleading unless these other

qualifications are known.

All

these difficulties in measuring work progress, whether based on the project's

expenditures or installed quantities, led into the development of the earned

value concept. The earned value is the amount budgeted or planned to reach a

specific goal regardless of the actual expenditures incurred in reaching that

goal. Implementation of this concept is accomplished by identifying

distinguishable events (control points) throughout the life cycle of the work

items and by developing earning rules for reaching these events. The control

points for a work item such as placement of a footing foundation may include

excavation, forming, steel reinforcement, placing concrete, and backfilling. The

earning rules assign a value to each control point. The earning values can be

expressed as percentages of the item's budget, duration, or an arbitrary work

unit.

The

status of each work item is determined by determining whether or not the control

points were accomplished. The work item earns the full percentage assigned to a

control point only when it is completed, but partial credit may also be allowed

if appropriate. The work progress (percentage of completion) and the earned

value for a work item are determined by the following Equations:

![]() Equ.1

Equ.1

![]() Equ. 2

Equ. 2

Where:

(PC) is the percent complete for the work item under consideration, (CPi) is the

earning percentage associated with control point number i, and (Ai) is the

actual progress accomplished on control point number is expressed in percent.

To

determine the progress at a higher level on a WBS, for example, the entire

foundation, one adds the earned value of all footings and divides that total by

the total budget for the entire foundation. This computation is expressed by the

following Equation:

![]() Equ. 3

Equ. 3

It

should be noted that Equation 3, which is another form of Equation 2, is

applicable at all levels of control on the WBS.

Cost

and Scheduling Integration

The

WBS is also considered the key to the integration of cost and scheduling data

[4].

This integration can be achieved by developing a WBS in which the work items represent scheduling activities, and by assigning a unique cost code to each level of control on the WBS. By doing so, costs of each scheduling activity can be tracked for control purposes, and integration of cost and scheduling can be achieved.

PROBLEMS IN CURRENT APPROACH

Although

the two management challenges may appear to be well under control, in reality

they are not. Hidden problems still exist which limit the application of the

various concepts presented. These problems involve both the level at which

cost-scheduling data are integrated and the basis for progress measurement.

Level of Cost-Scheduling Integration

If

a work item on the WBS presents a typical scheduling activity (e.g., place draft

fan foundation, erect retaining walls, etc.), it may not satisfy the

requirements for being a typical cost item. Cost items in a project budget are

not activity oriented. Unlike the scheduling activities, cost items (e.g., site

work, concrete, finishes, equipment, etc.) and their cost codes are material or

craft oriented. It is the common practice that budgets follow the estimates'

format, and cost estimates are not usually structured around a WBS. Estimates

customarily follow the Construction Specifications Institute (CSI) MASTERFORMAT

or a similar format. Cost records, therefore, are not usually available at the

level of detail appropriate for full integration with scheduling activities.

To

further illustrate, a scheduling activity (e.g., placing a footing foundation)

involves several subactivities (e.g., excavation, formwork, reinforcement steel,

concrete work, hardware, installation, and backfilling operations). Each

subactivity belongs to a different cost item. The cost of each subactivity is

only a small component of a major cost item, for which cost records are not

readily available.

Although

theoretically nothing prevents us from keeping costs at any level of detail,

practically costs are not kept at the subactivity level. An attempt to keep cost

records at the subactivity level will result in creating an unmanageable cost

system and imposing unnecessary extra work on the material handling system.

Basis for Progress Measurements

With

the above in mind, a question arises on whether progress should be based on

cost, time, or other basis. In other words, when a project is reported 70%

complete, does this mean that 70% of the budget was rightfully earned, the

project will be completed after a duration equal to 30% of its planned duration,

or 70% of the quantities were placed ? Another question then becomes obvious:

what are the relationships between the percent complete, budget, and duration of

a construction project ?

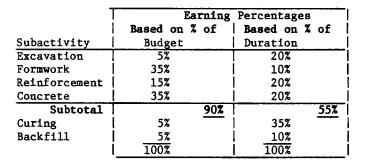

The

progress status of an activity and likewise of a project may vary significantly

depending on the basis for measurements. Table 1 illustrates numerically the

variance in work progress for a footing foundation reported on different basis.

Assuming

that work was completed on the first four subactivities at the time of update,

the reported progress could then be equal to either 90% if progress is based on

cost or only 55% if based on time.

| TABLE

1. Reported Progress of a Work Item |

|

|

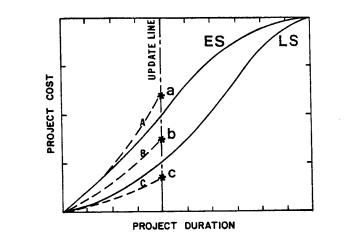

| FIG.

2 - Time-Cost Envelope Diagram |

Further

analysis of the three possible actual performance curves suggests that none of

these interpretations is conclusive and each could be misleading. Points 'a',

'b', and 'c' could each depict a poor performance or an excellent performance.

Point 'a', for example, may indicate cost overrun, but it could also indicate

excellent performance resulting from accomplishing more work than scheduled; or

it could reflect early arrival of either material or equipment for which cost

was reported earlier than anticipated. Similarly, point 'c' may indicate slow

progress which is reflected by a cost underrun situation, or it may mean

excellent performance resulting from getting work accomplished under budgeted

cost. Conversely, point 'b', the supposedly desired and acceptable performance,

may in reality be the result of poor performance if it meant the same progress

represented by curve 'C' but achieved at a higher cost.

In

recognition of these shortcomings and in an attempt to improve this widely used

management tool, a modification was recently proposed in 1986 (5].

The

modification recommended plotting the project's cost profile and the project's

accomplishments curve on the same graph in a manner similar to that shown in

Figure 3.

|

| FIG

3. Modified Time-Cost Envelope Diagram |

Assuming

that work was completed on the first four subactivities at the time of update,

the reported progress could then be equal to either 90% if progress is based on

cost or only 55% if based on time.

PROBLEMS IN REPORTING PROGRESS

The

time-cost envelope diagram is one of the most popular reports to describe the

progress of a construction project. This diagram is a graphical representation

of cost profiles based on early start (ES) and late start (LS) schedules, as

shown by the solid curves in Figure 2. As a project progresses, actual project

costs are plotted on the graph as indicated by the dashed curves. When a project

is represented by a curve similar to curve 'B', i.e., falling inside the planned

cost envelope, the progress of the project is judged to be satisfactory. If the

actual costs are described by curves similar to 'A' or 'C', outside the planned

cost envelope, the progress of the project is judged to be unsatisfactory. Curve

'A' is interpreted as an indication of an overrun situation, while curve 'C' is

interpreted as an indication of a behind schedule situation.

To

determine scheduling performance in this method, one projects point (a) of the

Actual Accomplishment curve onto the Scheduled Accomplishment curve (point b).

If this requires going back on the time scale, the project is behind schedule.

The expected delay is equal to the distance between point (a) and point (b) on

the time scale. In arriving at point (b) if it is required to advance ahead of

the update time, the project is ahead of schedule. The scheduling gain is equal

to the distance between point (a) and point (b) on the time scale.

A

cost overrun situation is detected by comparing the cost corresponding to the

level of accomplishments projected on the Cumulative Budget curve (point c) and

the actual cumulative cost at the time of the project's update (point e). If the

actual cost expenditure (point e) is greater than the planned cost (point c), an

overrun situation is detected. The magnitude of such a cost overrun is equal to

the difference between the two points (c and e) on the cost scale. Similarly, if

the actual cost expenditure is less than the planned cost, an under run

situation is detected. The magnitude of a such cost under run is equal to the

difference between the two points (d and e) on the cost scale.

Although

this modification offers an improvement to a widely used reporting method,

certain shortcomings remain. The modified approach still erroneously assumes

that a sound quantitative method exists for measuring work progress upon which

the performance curve is generated.

PROPOSED APPROACH

The

problems discussed above are perhaps a result of the current management approach

which in essence attempts to use one indicator in describing the performance of

an entire project. In effect, each point on the Cost-Time diagram is attempting

to describe performance in terms of cost, schedule, and completion

simultaneously. The inadequacy of this approach prompted the authors to search

for an alternative in which more than one indicator are used simultaneously to

describe the different aspects of progress, an alternative that is not based on

full cost-scheduling integration.

It

was interesting to notice the similarities and differences between how

construction projects are managed and how financial analysts manage business

enterprises. Financial analysts have been successful in evaluating companies'

performance and identifying problem areas using financial ratios. With this

technique, ratios describing the relationships among different items on the

balance sheet and profit and loss statements are used as indicators of the

overall performance of a firm. The emphasis is placed on understanding that none

of the ratios individually is a good indicator of a firm's performance, rather,

the value and correlation of many ratios collectively determine the business

performance [6,7]. Instead of searching for one indicator to describe the

success of the entire business, up to fifty different ratios are generated to

evaluate each aspect that affects the overall performance.

Another

important concept in this technique is the use of ratios of data elements

instead of the absolute values of such data. The use of ratios was found to

eliminate problems in comparing companies of different sizes or in different

locations. Also, the use of ratios expedited the analysis, reduced the large

numbers of items to a relatively small set of readily comprehensive and

economically meaningful indicators, and minimized the problems of time lag in

reporting costs [8,9].

Developing

a progress evaluation technique for construction projects which is analogous to

the financial ratios analysis technique is an alternative that deserves further

investigation. The development should address: 1) identifying project ratios

capable of describing the different aspects of work progress; 2) developing a

procedure to detect work items with potential problems; and 3) devising an

analytical algorithm to calculate the monetary impact on the final project cost.

CONCLUSION

Examination

of the current approach for progress evaluation indicated that major

implementation problems exist. Namely, these problems are in determining the

basis for progress measurements and the practicality and the degree of

cost-scheduling integration. This may result in generating misleading

information such as that reported by Time-Cost diagrams.

It

is suggested that a different approach to measuring and reporting work progress

is needed. Development of a methodology analogous to the financial ratio

analysis method which has been used in evaluating the performance of businesses

appears to be a promising alternative.

APPENDIX 1.-REFERENCES

|