-

- A Comparative Analysis of Financial

Statements of General Contractors

-

- Syed M. Ahmed, Ph.D., Weihua Mao, Aarti Pandit, and Juan Zheng

- Florida International University

- Miami, FL

-

-

Construction companies are shown by noted

agencies to have an alarming rate of business failures and bankruptcies. As

most construction companies are involved in large amounts of investments,

there are huge financial risks involved in these projects. The importance of

sound financial management of these mega-scale projects and the companies

executing such projects should not be under-estimated. In order to stress the

importance of financial management in the construction industry, two companies

were selected for this study. Certain relevant ratios were then selected for

carrying out a detailed ratio analysis. In addition, weights were assigned to

selected ratios, depending on their importance, to arrive at a single final

value for each company through simple mathematical calculations. Final

conclusions are then drawn accordingly.

-

-

Key Words:

ratio analysis, financial statements, construction companies, general

contractors, financial risks.

-

-

- Introduction

-

- Data from

noted agencies like Dun & Bradstreet, the Surety Information Office and the

Centre to Protect Worker's Rights, have shown that construction companies have

an alarming rate of failure, perhaps more so than companies belonging to other

industrial sectors. The basic function of these construction companies is to

execute and manage construction projects, a majority of which are on

mega-scales, involving capital investments in millions and billions of

dollars, and requiring several years for completion and return of investment.

Hence, the financial risks involved with these projects, which get transferred

to the companies working on them and from them onto the financial institutions

or private parties funding them, are tremendous. The overall management,

planning, design and construction aspects of these projects become critical,

wherein even small mistakes can lead to heavy losses. Hence, the importance of

sound financial management of these projects should never be under-estimated.

-

- Construction

projects range from infrastructure projects (e.g. water supply, electricity

and sanitation networks, dams, electric and thermal power plants, nuclear

reactors, etc.) and transportation projects (e.g. road, waterway and railway

networks, tunnels, bridges, harbors and airports) to residential and

commercial construction projects. Good financial management, implications of

the related decisions and the skills required to successfully complete

projects on time, within budget and with sufficient profit, can be best

understood from the financial statements of companies dealing with especially

large projects, in which small differences in financial ratios can translate

into extremely large variations in the actual amounts pertaining to any

account. Hence, it was deemed beneficial to select the financial statements of

two of the bigger general contractors in the country, in order to carry out

the financial analysis.

-

- A comparison

can be made between, the financial statements of a given company and the

industrial averages for companies in the same industrial sector or for all

companies in general, the same company for two different fiscal years, two

companies in the same fiscal year, etc. The objective of this paper is to

compare the financial statements of two general contractors for the same

fiscal year. The value of a financial ratio will reflect the concerned

company’s performance in a given market and other external conditions. By

selecting financial statements of two companies for the same fiscal year, the

authors can assume that the market and other external conditions faced by

these two companies are similar and can therefore interpret these ratios as a

result of the companies' performances in response to these external

conditions. The companies selected by the authors for this analysis belong to

the same industry i.e. the Construction Industry. However, they do belong to

different industrial sectors. The authors are, therefore, also able to

ascertain that the way a company handles its assets and liabilities to

generate profit, is based on the characteristics of the industrial sector that

the company belongs to.

-

-

- Background of the Companies

-

- Granite Construction Company – GC

-

- Granite

Construction Incorporated is the parent company of Granite Construction

Company, one of the nation's largest heavy civil contractors and construction

materials producers. Incorporated in 1922 and publicly traded since 1990, it

is a member of the S&P 400 Index. Granite Construction Company serves both

public and private sector clients and is comprised of many well-coordinated,

highly professional teams of Builders located across the nation. GC are best

known for transportation infrastructure projects including roads, highways,

tunnels, bridges, mass transit facilities and airports. The company also

produces sand, gravel, ready-mix and asphalt concrete and other construction

materials. Unusual among large contractors, GC is equally effective at

building through its two operating divisions, the Branch Division (BD) and the

Heavy Construction Division (HCD). HCD is a major user of construction

equipment and has developed substantial expertise with large, complex

projects. The branches draw on these resources, which are generally not

available to smaller, local competitors. Conversely, the BD offices have

greater knowledge of local markets and provide HCD with valuable information

regarding larger projects in their respective areas, as well as providing a

source of aggregates.

-

- Centex Corporation – CC

-

- Centex

Corporation is the nation's premier company in building and related services:

Home Building, Home Services, Financial Services and Construction Services.

Established in 1950 in Dallas, Texas, with revenues exceeding $10 billion,

Centex is a Fortune 250 company traded on the New York Stock Exchange under

the symbol "CTX." Centex consistently ranks among "America's Most Admired

Companies" in its industry, according to FORTUNE magazine. The company has

approximately 17,500 employees located in more than 1,500 offices and

construction job sites across the nation and in the United Kingdom.

-

- Both these

companies are very big and comprehensive construction companies. However, both

focus on different types of construction projects. GC has more emphasis on

heavy infrastructure projects and construction materials production.

Comparatively, CC has more experiences on home building and construction

services. This difference will be considered in analysis and conclusions.

-

-

- Methodology

-

- Instead of

selecting the Financial Statements of small-scale General Contractors, two

premier construction companies Granite Construction Incorporated (GC) and

Centex Corporation (CC) are selected to find out what results can be expected

as normal, for companies in the construction industry, who are financially

sound or doing well. These companies are well-reputed and work on

mega-projects. Hence, their Financial Statements would be similar to what can

be considered as normal financial statements of companies in the construction

industry and hence will not give skewed results in the financial analysis.

-

- The Annual

Reports of the two selected companies, both in the same Form 10-K format, as

required by the United States Securities and Exchange Commission are used for

easy comparisons. These reports include the following financial statements,

Consolidated Balance Sheets, Consolidated Statements of

Income/Revenues/Earnings, Consolidated Statements of Stockholder’s Equity, and

Consolidated Statements of Cash Flows.

-

- The ratios

used for financial analysis are ratios specific to the construction industry.

The source for these ratios is Dun & Bradstreet, Inc., Industrial Norms and

Key Business Ratios One Year - Desk Top Edition. A financial analysis for a

specified fiscal year (GC-December 31, 2002 to December 31, 2003 and CC- March

31, 2003 to March 31, 2004) is carried out. There is a 3 - month lag between

the selected fiscal years of the two companies, due to a difference in their

financial policies. Since three-month escalation will not affect a company’s

ratio except the absolute value, this minor difference will be ignored for

convenience in comparison of the two companies, thus assuming that the two

sets of data correspond to the same fiscal year.

-

- If two

reports from two different time periods were selected, it would be difficult

to compare them, as the values recorded in these reports could have been the

result of very different market conditions. Using the financial reports of two

companies for the same time period, the results of their ratio analysis can be

used to indicate the companies’ performances in response to these external

conditions for the sake of comparison between them. All values, including

those from the balance sheet, have to be taken for a certain period and since

the balance sheet corresponds to an instant in time, the value from a balance

sheet entered into this ratio must be the average of the corresponding values

on two balance sheets i.e. that for the Start of the concerned Fiscal Year

(GC- December 31, 2002 and CC- March 31, 2003) and that for the End of the

concerned Fiscal Year (GC- December 31, 2003 and CC- 31st March

2004). The values from the income Statement correspond to the same period as

the selected fiscal year (GC- December 31, 2002 to December 31, 2003 and CC-

March 31, 2003 to March 31, 2004).

-

-

- Financial Ratios

-

- Financial

ratios are used to analyze the financial statements of the two companies. A

financial ratio is a ratio obtained by dividing one category or group of

categories on the given company's financial statement by another category or

group of categories on the same company's financial statement (Peterson,

2005). The ratio is expressed as a ratio to 1 (e.g. 0.2:1) or as a percentage

(e.g. 20%) or as the number of times an event occurs during a certain period

(e.g. number of times a company turns over its working capital). The financial

statements most commonly used for this analysis are the company’s balance

sheet and income statement. Although for some analysis, Statements of

Stockholder’s Equity and Statements of Cash Flows are used as well.

-

- Over a period

of several years, data collected from the financial statements of several

companies from each industrial sector has been analyzed in order to prepare

target ratios for each industrial sector. Corresponding to each sector,

statistical data analysis has also provided a median value and a range for

each ratio. This ratio enables the interpretation of the relationship between

the various values shown on the financial statement and to draw appropriate

conclusions from the same. The authors compared different ratios for these two

companies, obtained from calculations from its financial statement, with the

standard value for that ratio for the corresponding industrial sector. From

this comparison, several conclusions regarding the company's financial health

were drawn.

-

- Financial

ratio analysis will help the financial manager of the company to identify a

potential financial problem in the company before it becomes a crisis. It can

help handle simple planning issues, for example, setting aside funds to

account for the depreciation of a company asset, such as equipment, in order

to enable purchase of its replacement at the end of the life span of that

asset. It can also provide insight into the company's ability to pay bills,

efficiency in utilizing its financial resources, profitability, capital

structure of the company, as well as assist in analysis of other basic

business/financial functions.

-

-

- Analysis of Data

-

- Financial

ratios measure different aspects of a firm’s financial status. For better

comparison, ratios are analyzed in four major categories, liquidity ratios,

capital structure analysis, activity ratios, and profitability ratios.

Liquidity ratio measures the ability of the firm to pay its obligations as

they come due. Capital structure analysis measures a company’s ability to

manage debt and demonstrates the way a company has chosen to finance its

operations. Activity ratios measure how effectively a firm is using its

assets. Profitability ratios measure the ability of the firm to generate

income from operations and thus increase the equity (Jackson, 2002).

-

- Liquidity Ratio

-

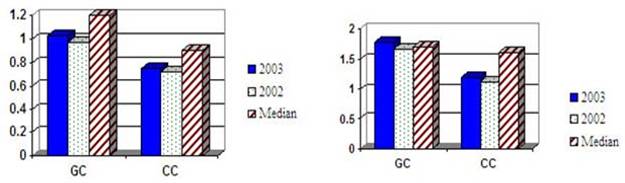

- Quick

Ratio & Current Ratio

[See Appendix “Ratio Analysis Table”]

-

- The quick

ratio and current ratio reflect the company’s ability to pay current

(short-term) liabilities, i.e. its short term liquidity. In 2003 and 2002,

GC’s Quick Ratio was 1.03 and 0.97 respectively, while CC’s was 0.75 and 0.72.

GC’s Current Ratios was 1.77 and 1.67 in 2003 and 2002 respectively, while

CC’s was 1.19 and 1.12.

-

- Fig. 1 shows

that both GC’s and CC’s quick ratios are slightly below the corresponding

medians for their respective industrial sectors. The quick ratios of GC in

2002 and CC in 2003 and 2002 were lower than 1:00 to 1, which means they were

both not liquid enough. Nevertheless, their quick ratios were well within the

range. Fig. 2 shows that both companies have the ability to pay current

liabilities because their current ratios are higher than 1.00 to 1.

Furthermore, GC’s current ratios in 2003 and 2002 were almost the same as the

typical current ratio for heavy and highway companies. It increased from 1.67

in 2002 to 1.77 in 2003. CC’s current ratios were lower than those for a

typical single-family residential company not only in 2002, but also in 2003,

but within the range. Although CC did some improvement from 2002 to 2003 for

its short term liquidity, its current ratio was still not very good. According

to their current ratios, GC performed better than CC. CC was probably

undercapitalized and could have run into financial problems during the next

year as its ratios were below 1.50 to 1.

-