(pressing HOME will start a new search)

![]()

![]()

- ASC Proceedings of the 23rd Annual Conference

- Purdue University - West Lafayette, Indiana

- April 1987 pp 53-56

|

(pressing HOME will start a new search)

|

|

TEACHING

PROJECT CASH FLOW PROJECTIONS USING A SIMPLE SPREADSHEET

|

Edward

H. Keeter |

|

Project cash

flow projections can be successfully taught using either manual or

computer generated projections. This paper describes a method for

teaching project cash flow projections using a simple computer generated

spreadsheet. Some of the advantages of using a computer are: student

time is spent in analyzing the cash flow budget rather than in manual

computations, the ability to manipulate the spreadsheet can be used to

solve other construction problems, and the student's work can be easily

graded. An IBM-XT computer and Lotus 1-2-3 software was used to generate

the spreadsheets described. However, most personal computers and

spreadsheet software are capable of producing the examples used in this

paper. |

INTRODUCTION

The

process of managing a construction project is complex. General contractors take

responsibility for an entire project but subcontract out most or all of the

actual construction to specialty contractors. The size and uniqueness of the

product, the impermanence of relationships, and the overlapping control

mechanisms of the participants require a considerable amount of management

expertise to be exercised by the general. contractor. Management functions in

the construction process must entail, therefore, a full range of contractual

tasks such as purchasing, fabrication control, inventory control, personnel

supervision, and contract management.

Despite

the sophistication with which some of these firms perform managerial tasks, the

size and complexity of construction projects often outpaces the capacity to

manage all aspects of the construction process effectively. As a consequence,

the construction industry experiences an inordinate number of business failures.

It is well known that entry into the construction business is relatively easy,

requiring little preplanning or capitalization. Exiting, frequently via

bankruptcy, is also very easy. Business failure in the construction industry can

usually be traced to poor management skills rather than to a lack of technical

competence or to the failure to demonstrate mastery of the respective

construction trades.

According

to Dun and Bradstreet, the top three reasons for construction firm business

failures are: lack of business experience, inadequate project estimating and/or

cost control, and inadequate working capital. The third reason for failure,

inadequate working capital, is mainly a problem of poor cash management. In

poorly managed firms, cash management is frequently neglected and insuring that

enough cash is available at the right time becomes a daily problem. This is

unfortunate and unnecessary since, assuming that a project is priced and

controlled properly, most contract payment terms enable a contractor to produce

an adequate cash flow without the daily or weekly need to "scramble to make

ends meet and pay bills".

The

successful contractor plans for the maintenance of adequate cash balances so

that his company can operate efficiently, pay debts on time, and take full

advantage of cash discounts. In most cases a company's cash flow projections

will determine the amount and quality of jobs that can be safely undertaken.

Since most banks and sureties consider contractors relatively high risks, the

amount of financing available to finance operations and the contractor's bonding

limits are determined, in large part, by an analysis of working capital and cash

flow.

CASH FLOW PROJECTION

The

major purpose of projecting project cash flow is to determine how much and at

what time in the construction cycle cash will be needed to finance operations.

If money has to be borrowed to finance operations, the creditor wants to know

why, when, and how much the contractor needs to borrow. In addition, the

creditor will demand to know how and when the money will be repaid. If the

contractor must supply bonding, the surety will demand to see cash flow

projections that will allow him to determine if the contractor's line of credit

is sufficient to finance the volume of work to be bonded.

In

addition, most construction contracts, such as AIA 201, require the contractor

to supply the owner with a schedule of values that will be used as a preliminary

basis for payments to the contractor. Cash flow can be characterized as

"cash-in/cash-out".

The schedule of values required by the contract is simply the contractor's

estimate of "cash-in" timing.

There

are two levels of cash projections that concern the contractor. The first level

is project cash flow projection. This is an estimate of cash flow over the

contract life of each project. The second level is company cash, flow

projection. This is a summary of the combined cash flow for all projects and the

indirect, administrative, and financing expenses of the company. This paper will

address the development of project cash flow projections.

Project Cash Flow Projection

The

basis for plotting the cash-in and cash-out for a construction project is the

project schedule or plan and the estimate summary sheet. At the very least the

contractor must know the starting and ending dates of each activity and the

direct and indirect costs of each activity. This information is essential to

managing the cash that flows in and out of a project.

In

addition to the schedule and estimate the contractor must know what conditions

the contract has put on progress payments. This information will determine when

and how cash flows into the project.

The

estimate, project schedule, and progress payment schedule information must be

combined with company policies concerning payment of labor, subcontracts,

equipment, and materials. The project cash flow projection can then be prepared

based on when the costs will be payed (cash-out) and when payments will be

received (cash-in).

TEACHING PROJECT CASH FLOW PROJECTION

Teaching

construction students the fundamentals of projecting project cash flow can be

tedious and time consuming. Before computers became common classroom tools, cash

flow analysis using manual computations was necessarily cursory. The use of

computers allows the student and the instructor to focus on the concepts of

managing a construction company's cash rather than focusing on developing

procedures to prepare a cash flow budget. The following sections will describe

how a simple computer generated spreadsheet can be used to teach cash flow

concepts to construction students in a senior project management class.

Course Description and Environment

The

class in which cash flow concepts are taught at East Carolina University is a

senior level class in project management. The class is the third in a sequence

of courses designed to simulate the construction phase of the building process.

The course emphasis is on the application and practice of management techniques

to control the manpower, materials, money, and machinery of a construction

project.

The

students entering the class are typically seniors in the Department of

Construction Management who have completed most of the management and

construction courses required in the program. They should have completed

estimating and scheduling as well as management courses such as accounting,

finance, and personnel management. In addition, the students have usually

completed at least one computer course which introduced them to the use of a

personal computer and related software.

Since

the class format is primarily lecture/discussion, all of the hands-on computer

time is spent outside of class. The Construction Management program is not

blessed with unlimited funds and facilities. Consequently, the class must use

computer facilities located in another building. These facilities are very

adequate and readily available at most times. If the computer rooms are to be

used for classroom instruction they must be reserved ahead of time.

Computers and

Software

The

computers available to the students are primarily IBM PC's and Apple IIe's and

Macintosh's. The students are allowed to choose the type of computer they wish

to use. This decision is usually based on which computer was used in the

required computer course; usually IBM PC's. However, some students either own

other makes of computers or would rather use an alternate computer.

There

is a wide range of software available to the students. If the students have

completed the required introductory computer course, they have already purchased

an integrated software package written for the IBM PC. In addition, the student

may check out, many different types of commercially available spreadsheet

software.

The Assignment

Cash

flow concepts are usually introduced in the fourth to fifth week of the

semester. After approximately two hours of lecture devoted to describing the

cash flow projection process, the students are asked to develop a spreadsheet

template which will allow monthly cash flow projections for a simple project.

This template is produced manually and checked for accuracy and its ability to

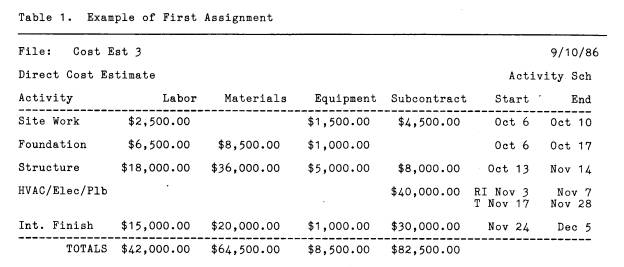

produce the desired results efficiently. Table 1 is an example of the assignment

given to the students.

|

|

When

development of the template is complete, the students are assigned a more

complicated project that requires them to use spreadsheet software to determine

cash flow projections. The assignment consists of an Estimate Summary and

Preliminary Project Schedule (start and end dates only) of a small office

complex that priced out at $497,000 The assignment is done outside of class and

is due in two weeks.

To complete the assignment the students are required to turn in a cash flow analysis that displays when costs are to be paid, when payments are received and what financing must be available. The only manual calculations required to complete the assignment are used to determine when the student wishes to pay for labor, materials, subcontracts, and equipment. In order to keep the analysis simple, certain assumptions must be made. These assumptions are:

1.

Payroll is paid weekly.

2.

Materials are purchased at the start of an activity. They must be paid for by

the 10th of the month after installation in order to receive a 2% cash discount.

3.

Subcontracts must be paid by the 15th of the month for work completed the

preceding month.

4.

Equipment rental is paid by the 10th

of

the month after use. 5. Company overhead is 15%. 6. Profit is 10%.

7.

Interest is 10%.

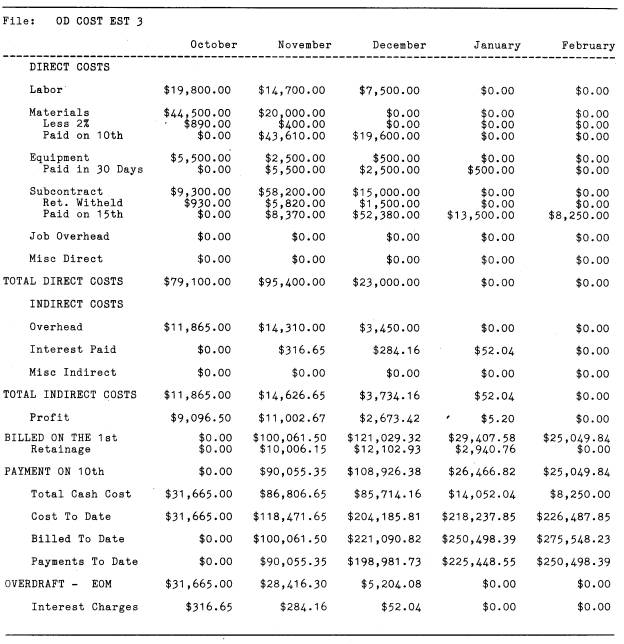

Table

2 presents the typical analysis sheet turned in by students.

|

Table

2. Example of Completed Assignment |

|

|

The

final unit of instruction describes how to project the cash flow analysis to

monthly balance sheets, statements of earnings, and company cash flow

projections. Since time is a factor, this procedure is demonstrated.

CONCLUSION

There

are many advantages to teaching project cash flow projections using computers

and related software. Probably the most important advantage is that it requires

the student to solve problems by creating solutions (spreadsheets) rather than

simply determining the correct number to plug into a prepackaged solution.

Though there are many excellent software packages available, many require little

of the student except to "walk through" the program. Many software

packages that claim to estimate, plan and schedule construction projects are, by

necessity, designed to fit a broad range of situations. A student using this

software spends most of his time trying to mold his situation into the

parameters of the software rather than molding the software to solve the

problems created by his situation.

Another

important advantage is that the student can use the spreadsheet skills he has

learned analyzing cash flow to solve other construction related problems. The

analysis of equipment needs and crew level planning are two of the areas readily

adaptable to spreadsheet analysis.

Finally,

the students' and the instructor's time is used more effectively. Students can

spend more time determining the solution to the problem rather than performing

lengthy, though simple, calculations. The instructor saves valuable time in

grading and creating new assignments. It is very easy to modify the assignments

and the templates required to solve problems. The time saved by the instructor

is well worth the investment in learning to teach cash flow using computers and

spreadsheets.